CAC 40

CAC 40

A question of style

What is a defensive case, as opposed to a cyclical case? Basically, identifying candidates is like answering the question "which expenses do I renounce and therefore which ones are incompressible, as a consumer or as a business leader?" For example, an individual will continue to feed himself, to take care of himself, to subscribe to water, electricity, telephone and will continue to put gasoline in his vehicle. On the other hand, it is likely that he will postpone the purchase of a new vehicle, the work on his house and that he will be more careful with his trips abroad or his outings to the restaurant.

For the purposes of this piece, we will refine the sectoral reading a little bit by using four indices in addition to the Stoxx Europe 600 (the broad European index, which counts 600 stocks as its name suggests). The STOXX proposes a slightly more detailed classification into four "benchmarks": cyclical, defensive, consumer staples and consumer discretionary:

• True defensives follow their course almost independently of economic cycles. They are more resilient when things go sideways but have little leverage when the economy is operating at full capacity.

• Societies classified as basic consumers are not unaware of economic cycles, but they are not very sensitive to them.

• Cyclical companies follow major economic movements: they earn more money when growth accelerates and less when it slows down.

• Companies in the consumer discretionary universe benefit from significant leverage during periods of growth.

The features of each classification

The STOXX Europe 600 Optimised Defensives (SDEFN) includes 113 stocks that are slightly dependent on the evolution of the cycle, including 46% in Health, 20.2% in Oil & Gas, 15% in Utilities, 13.8% in Telecoms and 5.1% in Insurance. The small insurance pocket is mainly composed of reinsurers.

The STOXX Europe 600 Optimised Consumer Staples (SCOST) consists of 41 companies offering basic consumption, moderately to minimally sensitive to cycles. It is 46% dominated by Personal Consumer Products and Home Care and 41.5% by the Food & Beverages segment. The remaining 12.5% is distribution.

The STOXX Europe 600 Optimised Cyclicals (SCYC) is an index that incorporates securities that are well correlated with economic cycles. Much more extensive (309 components), it contains 29% banks, 23% capital goods, 10.4% insurance, 8% technology, 7.9% basic resources, 6.3% chemicals, 5.2% construction, 4.2% financial services, 3.5% real estate and 1.4% oil and gas. The Oil & Gas portfolio concerns exploration and service companies and no longer majors as in the defensive index.

The STOXX Europe 600 Optimised Consumer Discretionary (SCONDR) includes 84 companies in the "Discretionary Consumer" universe. Automobile & Equipment Manufacturers (27.3%), Personal Consumer Products and Home Care (25%), Media (19.9%), Specialised Distribution (14%) and Leisure (13.8%).

To avoid making the subject too cumbersome, we will only scratch the surface of the delicate debate surrounding the classification itself, which calls for comments and which differs from one provider to another. Why should an Eutelsat be classified as a media company rather than a telecom company? Should L'Oréal belong to the discretionary universe instead of the Consumer staples? Does the length of the aeronautical cycle still make Airbus a cyclic? Where to store an Amazon or a Google (not in Europe anyway, you might say)? In short, no classification is perfect.

What pays the most?

To return to the case in hand, let us look at the four strategies and the Stoxx Europe 600 across four periods:

-In 2018 (from January 1 to October 10)

-Since the French index CAC40 high point before the subprime crisis (June 1, 2007)

-Since the low point of the CAC40 after the subprime crisis (10 March 2009)

-Between June 1, 2007 and March 10, 2009, the worst investment timing in recent years

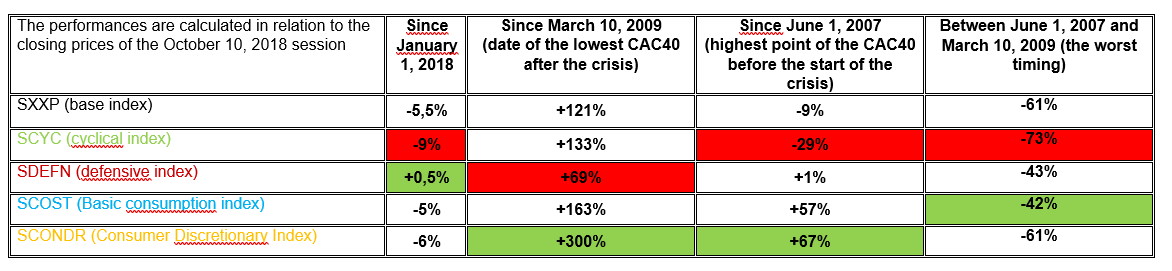

The table below shows the performance of each classification over the three periods, with the worst and best strategy for a given time step in red and green (click to enlarge):

• In 2018, being defensive paid off a little, while the cyclical pocket shows quite clearly the worst performance.

• The investment champion who would have entered the market at the lowest level in 2009 had every interest in betting on discretionary consumption (+300%), while the defensive strategy is logically on the decline (+69% only)

• The investor who had the misfortune to enter the market at the highest level on June 1, 2007 would not have had the best performance by betting on defensive measures, but he would have limited the damage. Once again, discretionary consumption dominated (+67%), while pure cyclicals were at a loss (-29%).

• At the heart of the crisis, cyclicals have been laminated, particularly because of financial stocks. The lowest losses were recorded in basic consumption, which beat the pure defensives by a slight margin.

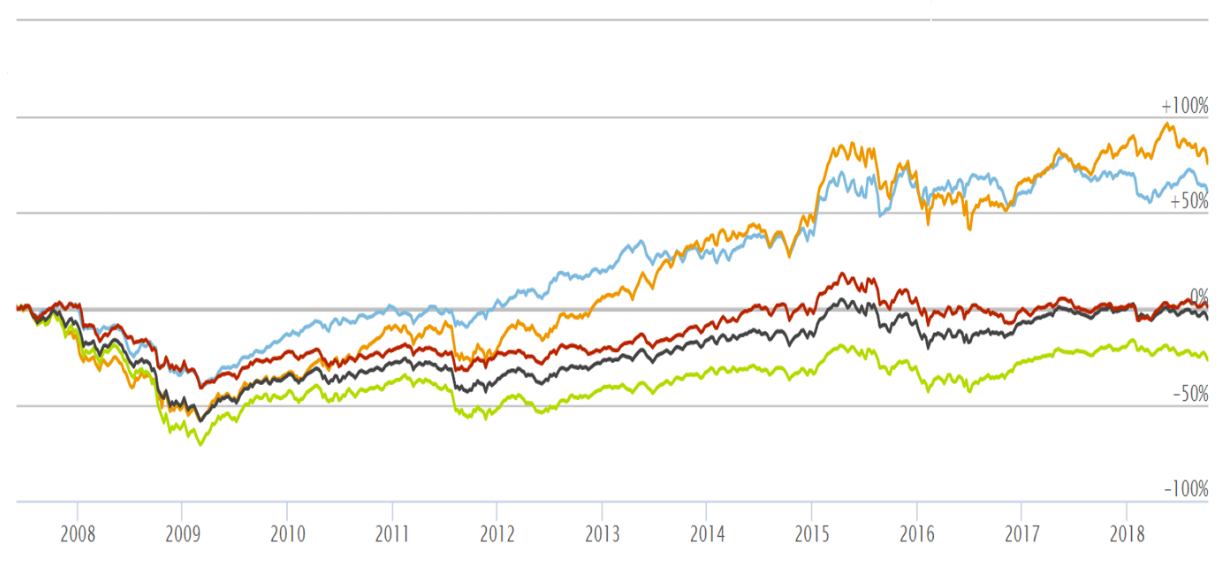

The performances since June 1st, 2007, in graphs (the color code corresponds to the table (Source Stoxx.com - Click to enlarge)

These performances show that the consumer discretionary pocket is by far the most attractive over the bull cycle period that began on March 10, 2009. But it also dominates by integrating the plunge of the 2007/2009 period, even if betting on basic consumption was also a relevant alternative. On the other hand, going defensive and staying defensive was not an interesting option, because although the shock was cushioned during the subprime crisis, the pocket did not have a spring during the long bullish phase. The only consolation is a better resistance this year. As for the cyclical pocket, it comes last in three of the four configurations, even if the underperformance was increased by financial stocks, the main victims of "subprimes".

A refined reading to come

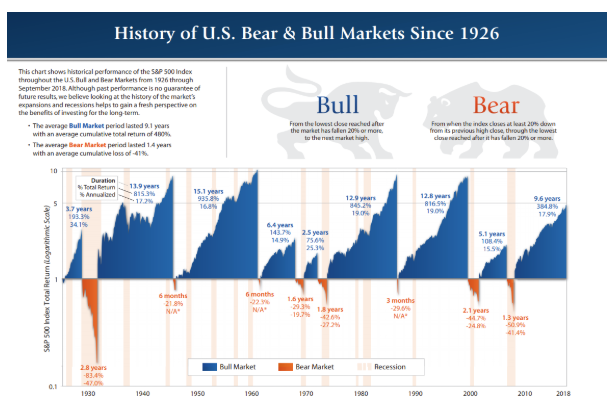

In a future development, we will talk in finer details about the major forces that explain the different variations, in particular the sub-sectors and values that have fueled these performances. We will also look at the stocks that have had the best returns over 20 years – taking in account the 2000 Internet crisis. We will also add the dimension of dividends, far from being negligible over such periods. One should keep in mind that periods of stock market crisis are infinitely shorter than periods of expansion, as shown in the graph below by First Trust.

A refined reading to come

In a future development, we will talk in finer details about the major forces that explain the different variations, in particular the sub-sectors and values that have fueled these performances. We will also look at the stocks that have had the best returns over 20 years – taking in account the 2000 Internet crisis. We will also add the dimension of dividends, far from being negligible over such periods. One should keep in mind that periods of stock market crisis are infinitely shorter than periods of expansion, as shown in the graph below by First Trust.

(Source : First Trust – Click to enlarge)