Fundamental Forecast for Pound:Neutral

- Interest rates have been key to the sterling’s performance, which is seen in its strength vs JPY and weakness vs NZD

- With the yield forecast so high, each piece of data can undermine bullish hopes

- Follow up-to-the-minute updates on the GBP via the Real-time Forex Newsfeed, and see GBP trade signals in DailyFX-Plus

The British pound offered up an unflattering performance this past week. While the currency was unable to mount a meaningful advance, neither would it loose substantial ground against most counterparts. Stability in exchange rates is sought by central bankers but not currency traders. Looking out over the coming week, the question is whether there is enough of a tide to drive the sterling to a revive the bullish trend that flourished from this past summer until February or the spark that sends the currency tumbling.

Before plotting the sterling’s course, it is important to appreciate its current bearings. Since the UK economy started to show evidence of turning around and current BoE Governor Carney stepped in with a more hawkish message, the currency has appreciated against all of its counterparts with the exception of the New Zealand dollar (whose central bank has actually hiked rates). With a modest loss against a high-yield and aggressive carry counterparts like the kiwi to substantial gains against the dovish Canadian dollar (GBPCAD is up 12.3 percent) or stimulus heavy yen (GBPJPY 11.4 percent), it is clear what matters most for the pound: yield forecasts.

In the risk spectrum, the pound carries enough of a safe haven appeal to compete with major liquid counterparts; but its market rates are material enough to keep it out of the ‘liquidity of funding currency only’ category. According to short-term rates markets, the market seems to pin the first Bank of England rate hike around March of 2015. That is well ahead of the Fed, RBA, ECB and Bank of Canada.

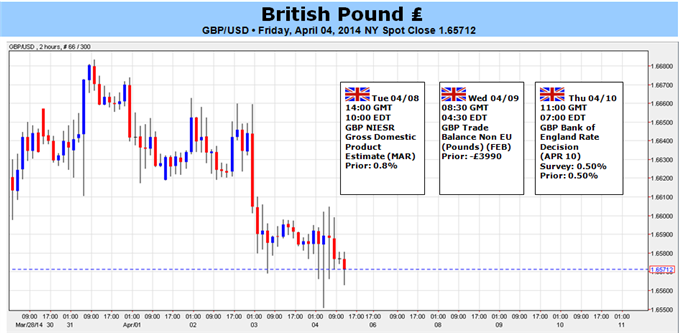

Maintaining that hawkish/bullish outlook until that first move is realized is the difficult part. At current levels, the market’s assumptions for rates are high. To maintain current levels – much less gain further ground – we would need to see an improvement in economic activity and material return of inflation pressure. We will find updates on both fronts with this week’s data – likely offering the market more to work with than the Bank of England decision scheduled for Thursday…

For economic updates, we have data that will cover employment, factory activity, trade, housing and a general growth assessment. Of the reports, the NIESR GDP Estimate for March is most comprehensive. While this data is afforded relatively little attention (or at least short-term volatility), it maintains a particularly good and leading relationship to the official GPD statistics. Furthermore, given an increased scrutiny over data that shapes rate decisions, this report could be afforded more respect.

Economic strength is key to ushering in a return to rate hikes, but what truly necessitates such a move is inflation. While we don’t have the CPI figures until the following week, we do have the RICS house price measure and the BRC’s Shop Price Index – which is a very good proxy for the official ONS consumer reading.

Assessing rate expectations through sterling activity alone or through sheer will of analysis is difficult. Sterling traders should be particularly attuned to the government bond (Gilt) yield curve. Should the market grow increasingly certain of a hike in the near future and further price additional tightening to follow in a regime, we will see it in rising yields in 2-year, 5-year and even 10-year bond yields. - JK

original source