From Covid through to mid-spring 2023, buoyed by pent-up demand and the healthy affluent classes, particularly in China, Europe's leading luxury houses outperformed the MSCI World by a wide margin.

In 2023, China began its economic downturn, and the country's rich portfolios no longer played their role as the locomotive of luxury. Inflation and the erosion of purchasing power in other major buying regions - Europe and the United States - were unable to offset the slowdown. Sales growth has fallen from 15% in 2022 to 11% in 2023, and is unlikely to exceed 8% this year (according to HSBC projections at the end of last year).

At the margins, sub-sector disruptions, new competition from the second-hand market, and a relative lack of appeal for certain brands have also played spoilsport.

Take Burberry and Ferragamo, suffering from the same ills. The aging brands (like their customers) are failing to win the hearts of the younger generation, and are suffering severe sales declines in North America and Asia-Pacific. Both have initiated strategic plans, store renovations and new management to breathe new life into their brands and dust off their reputations, to no avail. An interesting anecdote: the latter hired the former's CEO at the beginning of 2022 to carry out its reinvention.

The second half of 2023 was a difficult one for the British and Italian brands, crowned by a gloomy end-of-year holiday season. Earnings warnings followed, and analysts downgraded their recommendations on the shares. At Burberry, management was also criticized for pampering shareholders at the expense of investing in growth.

At Kering, the problem is similar, but accentuated by the preponderance of Gucci. The Group has relied too heavily on its flagship brand (which accounts for half of sales and two-thirds of operating income), which is losing momentum. Here too, a new Artistic Director, Sabato de Sarno, was to redefine the house's identity. He took up his post at the end of 2023, but has yet to provide the desired impetus.

For Compagnie Financière Richemont, parent company of Piaget, Jaeger-Lecoultre and Vacheron Constantin, the problem lies in a recent loss of interest in Swiss watches. After two years of growth, watch exports are suffering a marked slowdown: -3.8% in value and -5.2% in volume in February, again led by China.

The untouchables, LVMH and Hermès, Moncler and Brunello Cucinelli, although significantly affected by the weaknesses of their peers, fared better. LVMH relies on the great diversity of its brands, Hermès on its exceptional aura and Moncler on its specialization. Brunello Cucinelli, the little up-and-comer that makes ultra-luxury products exclusively in Italy, boasts sales growth of 24% in 2023. However, it has been marking time of late.

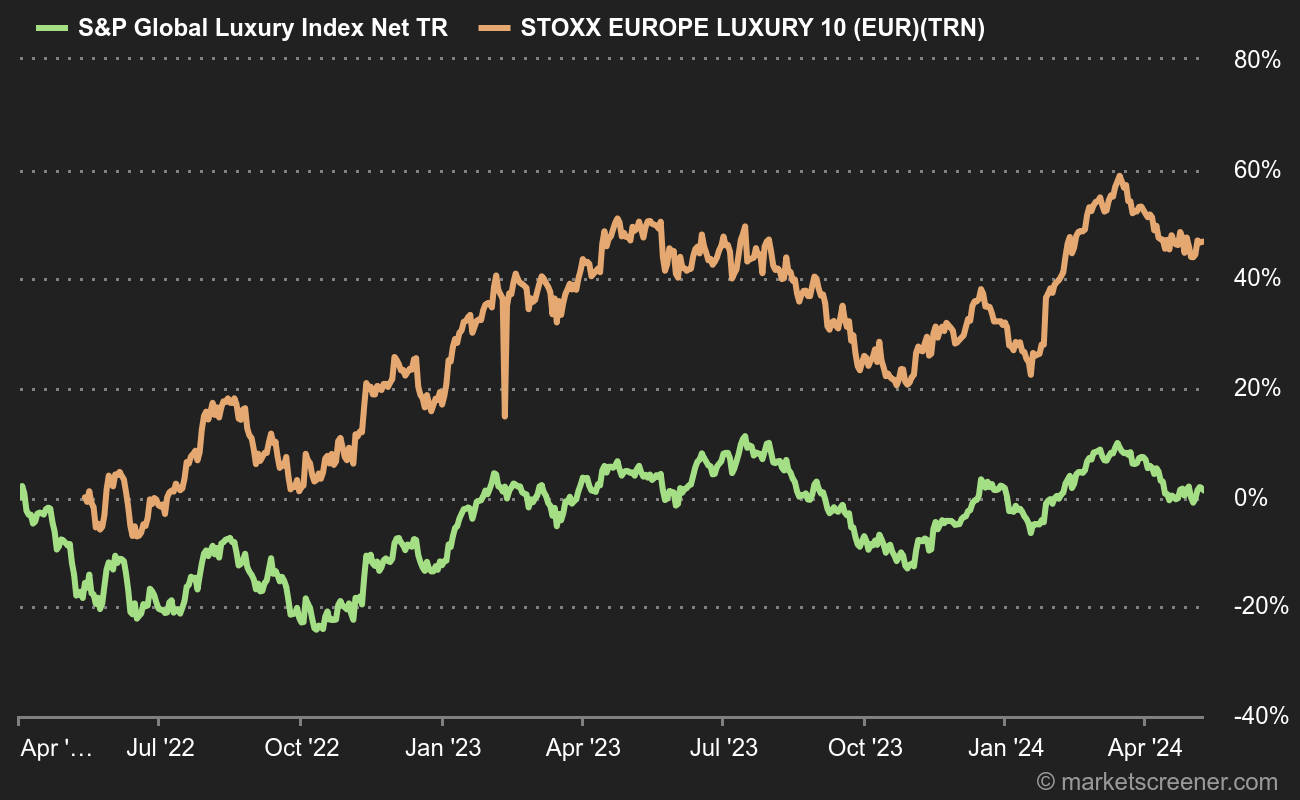

A reading of the S&P Global Luxury Index and the Stoxx Europe Luxury 10 is faithful to this narrative. The Chinese downturn of 2023 is visible, as is the recovery at the beginning of the year and the recent stall.