How can European banks cope with potential shocks, in an environment where Italy’s public debt is sky high and the UK is preparing to leave the European Union? This is what the European Banking Authority tried to gage during its toughest stress test yet, whose results were published on November 2.

The test covered 48 institutions, from ABN Amro to Unione di Banche Italiane Società Per Azioni. To carry out its task of monitoring the financial soundness of European banks, the EBA applied several more or less severe adverse economic scenarios to each institution to determine whether they will be able to withstand the shock in the event of a severe crisis.

Four systemic risks

The 48 banking groups represent 70% of the region's banking system. For the 2018 version of the tests, the institution has chosen as its adverse scenario:

-An unemployment rate of 9.7% in 2020.

-A cumulative decline in GDP of 2.7% over three years.

-Cumulative inflation of 1.7% over three years.

-A cumulative decline in residential property prices of 19.1% and commercial property prices of 20% over three years.

This framework is even more adverse than the scenario chosen during the previous test campaign. It incorporates the four systemic risks identified by the authorities: violent explosion of the risk premium, vicious circle on banking results, fears about the sustainability of public and private debt, liquidity risk in the non-financial sector.

Full CET1 ratio level above the minimum required

Of the 48 banks, 33 are part of the euro zone and the other 15 are based in Sweden, Denmark, Hungary, Norway, Poland and the United Kingdom.

The scenario includes four elements:

-Credit risk, including securitisation.

-Market risk, credit counterparty risk (CCR) and credit valuation adjustment (CVA).

-Operational risk (and risk management).

-Items included in one of the above categories: sovereign risk, money laundering risk, Brexit risk, IFRS 9.

All the establishments tested have a full CET1 ratio level above the minimum required of 5.5% in 2020 after being put under high pressure. The weakest links are Barclays (6.37%), Banco BPM (6.67%) and Lloyds Banking Group (6.80%). Among the ten lowest ranked institutions (CET1 full from 6.37% to 8.45%), there are two British, two Italian, two French, two German, one Spanish and one Austrian. With the exception of the two highest ranked banks, which are public institutions with special status (BNG Bank and NRW Bank), the reputation of Swedish banks is not usurped since they come at the top of the ranking, with ratios ranging from 21.98% to 16.47% for Swedbank, Svenska Handelsbanken, Nordea and SEB. The European average is 10.1%, according to the EBA.

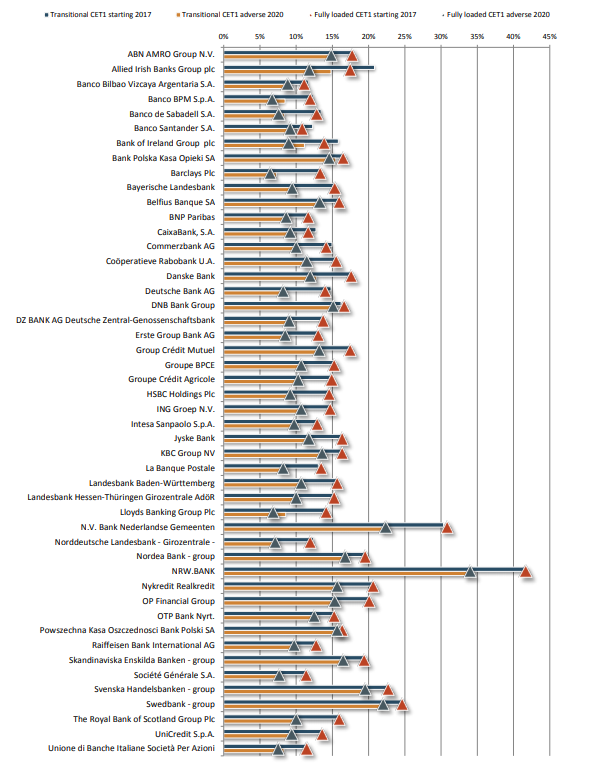

The graph below shows bank-by-bank CET1 capital ratios at the starting and end point of the exercise. It shows a large dispersion of banks’ capital position, both at the starting and at the end-point.

Source: European Banking Authority - Click to enlarge

Barclays and Llyods were the worst performers, which underscored the vulnerability of U.K. lenders to weak growth, credit losses and Brexit.

The British banks fared worse than German lenders such as Deutsche Bank AG and counterparts in Italy, which are grappling with a slump in the nation’s bonds amid turmoil sparked by its populist government.

However, analysts at Jefferies said the EBA stress test “has little impact”. It pointed out that “the UK banks fared the worst in the test due to macro risks associated with Brexit, but the results do not inform their capital requirements with the BoE publishing its stress test results on 5 Dec. With most of the controversial banks removed from the test this year, the results provide no surprises and we expect little market reaction.”