Mark Leonard is a fascinating person. He has built up a huge empire in the VMS (which stands for Vertical Market Software) sector over the last thirty years, very discreetly. A billionaire unknown to celebrity magazines. You won't find an interview with him, just a few photos on the Internet and that's it! His vision of entrepreneurship and his genius in the business world are, however, accessible to all through his annual letters to shareholders. These are real nuggets for managers, business leaders and investors alike. They detail his decisions, his vision and his approach to capital allocation.

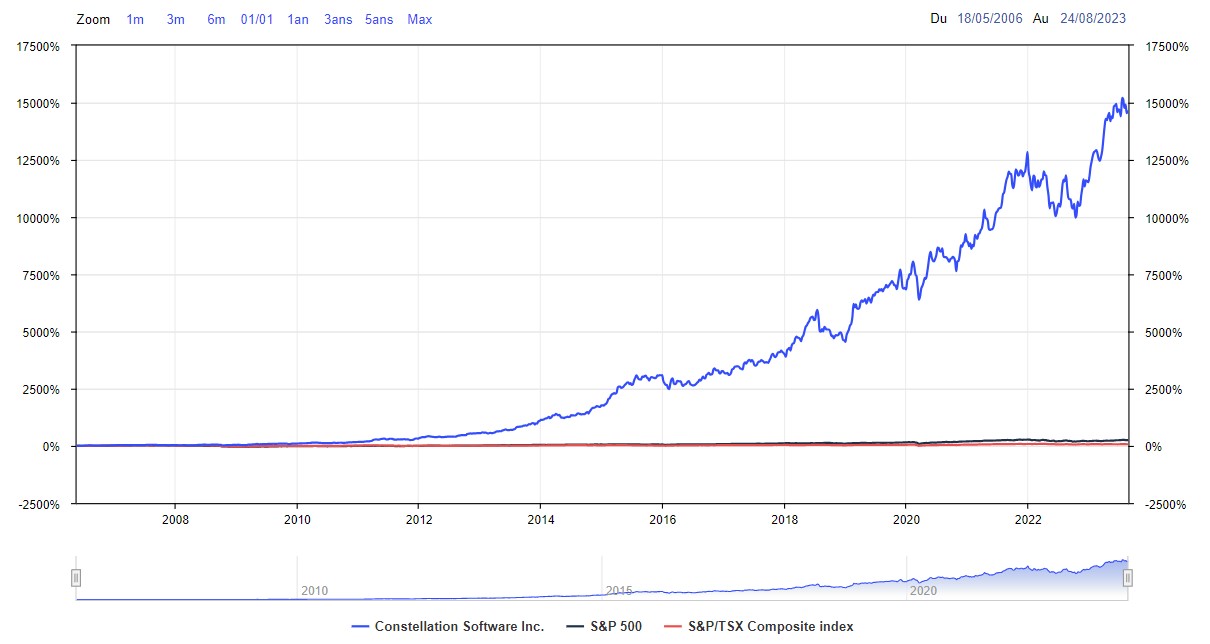

Price chart since the IPO :

Source : MarketScreener

Since Constellation Software 's IPO in 2006, the company's shares have multiplied by more than 156, representing an annualized return of 35.9% (dividends reinvested) since its creation. And operating results have been just as impressive as the share price. Return on equity has always been in excess of 30% per annum. A true example of entrepreneurial success. Let's take a look at this multibagger.

Year-on-year change in share price from 2006 to 2022:

Source : MarketScreener

Constellation Software, the other Berkshire Hathaway

Let's get back to Mark Leonard. He launched the company in 1995 and took it public on May 18, 2006. His absence from the media makes him a mysterious figure. In fact, in one of the only photos on the Internet, he looks like a wise man like Gandalf in Lord of the Rings or Albus Dumbledore in the Harry Potter films.

Mark Leonard started out in venture capital, and his mentor, Steve Scotchmer, taught him the importance of taking the long view in building an outstanding company.

Some of the highest-quality companies he identified were based on the VMS software model. That's what inspired him to move into this buoyant market. Vertical market software companies are essentially a type of software service that applies to a specific business or niche, whereas horizontal software (example: Microsoft Excel) can be applied to a wide variety of different businesses. In contrast, a vertical market software solution is created and customized specifically for an industry. These companies are generally in oligopolistic markets, and the players share the lion's share of the market, while posting higher margins, higher growth, are asset light and have recurring, stable revenues. A bit like the software sector as a whole... but better.

However, Mark wanted to differentiate himself from his new competitors: by setting much more ambitious targets for the level of quality he expected from the VMS companies he wished to acquire. He realized that his venture capital competitors were playing for the short term, whereas he wanted to find and keep the best VMS companies around for decades. Mark Leonard studied the career paths of great investors such as Warren Buffett and Charlie Munger, and wanted to invest for the long term, just like them.

In his annual letters (available here: President's Letters), Leonard talks about these VMS companies, how they maintain in-depth customer relationships and continually improve their products. So there's a very high level of trust with customers that's very difficult for competitors to replicate. So, even if a competitor tried to enter these niche markets with a similar product at a lower price, it wouldn't make sense for these customers to switch to the other company, because there's no way they'd be able to afford it. There's no reason to change supplier when everything's going well, and the budget associated with this expense is minimal in relation to overall costs. So, to sum up, these VMS companies are very high-quality companies, with a strong pricing power that really interests Mark Leonard.

So he thought he'd create a holding company that would specialize in acquiring VMS companies, and that's how Constellation was born in 1995. The holding company would acquire the VMS businesses. These VMS businesses would then generate cash flow for Constellation. At the same time, improve the company's operations, and thus profits, in order to buy even more new VMS businesses. Constellation generates high ROIC by infusing its acquisitions with the best practices of the business, bringing all the services and benefits of a scale-up holding company, and improving products and providing additional products to sell to their installed base.

The other advantage of the VMS market is the potential for added value from in-house improvements by its smaller companies. The return on investment is generally much higher than with the purchase of large or medium-sized companies. These smaller companies don't interest most venture capital managers, who don't waste time on companies worth a few million dollars. Mark Leonard has taken the opportunity to buy hundreds of companies, sometimes at less than one times sales or less than four times net income, in order to improve the efficiency of the units and then generate impressive results.

Leonard wanted Constellation Software to be a company that could be a permanent capital vehicle for the VMS industry, one where he didn't necessarily have to resell the acquired company. He left himself the option of keeping the companies as long as the synergies worked and the managers at their head saw an interest in them. In this sense, he is reminiscent of Warren Buffett. He doesn't speculate, he becomes a business owner and partner of the managers who run the company. Constellation now owns over 600 of these VMS companies, and has sold very few.

Recurring, well-diversified revenues

In terms of sales distribution, around half of Constellation's revenues come from government agencies, making their subscription revenues even more "sticky" and less subject to disruption from their competitors. Geographically, 10% of revenues come from Canada, around 50% from the USA, 30% from Europe and 10% from other countries. Given the number of customers spread across more than 600 daughter companies, customer diversification is important.

Source : MarketScreener

A decentralized organization

The company is organized on a decentralized basis, with a small head office and six operating groups supervised from there. Each operating group acts as a holding company to exit and acquire its VMS activities. Each of these operating groups is essentially what Constellation was in its early days. The aim is to decentralize responsibilities so as to have the same decision-making relevance as Constellation had at the start. The only difference is that, since the operating groups are part of the Constellation conglomerate, they get resources and support they wouldn't otherwise have.

The king of external growth

Historically, most of the company's revenue growth has been inorganic through acquisitions. Acquisitions are highly accretive. The minimum internal rate of return (IRR) is in excess of 20-25%, significantly better than the VMS industry. This may be explained by Mark Leonard's focus on free cash flow generation, return on invested capital, organic growth and software pricing power, rather than on growth at all costs, as some executives do.

With a median deal size of $3.3 million, we're talking about small companies. But not only: Constellation spent EUR 700M on its biggest acquisition. The small company market is more interesting because there is less competition on transactions worth a few million euros than on companies with capitalizations of several hundred million. Constellation holds a database of tens of thousands of such companies that would be considered potential targets, and this list continues to grow every year as more and more software companies are created and enter the space with these unique software solutions.

In January 2021, Constellation bought a spin-off of one of these operating groups called Topicus, which became a listed company doing much the same thing as Constellation Software, but in the highly fragmented European market. Discover a Topicus analysis here.

By 2022, Constellation had acquired 134 software publishers for a total of $1.7 billion. And just for reference, its market capitalization today is around US$42 billion.

Constellation Software 's reputation as a favorable place to sell a VMS business is another competitive advantage, similar to the reputation Berkshire Hathaway has built as a favorable place for founders to sell their companies.

A meritocratic corporate culture

Constellation is also a highly meritocratic organization that rewards dedicated employees. In 2015, over 100 employees had more than $1 million in company stock. The company's employee bonus plan requires all employees who reach a compensation threshold to invest a portion of that compensation in Constellation shares, which vest over four years. Between 25% and 75% of an employee's after-tax bonus must be invested in Constellation shares. In this way, remuneration is linked to the performance of the individual and the operating group, while wealth is largely tied to the success of the organization. Today, insiders hold almost 1.5 million of Constellation's 21 million shares. This pay-for-performance culture is attractive to many of Constellation's potential targets.

The best management team in the world? Perhaps, yes.

You have one of the most qualitative management teams in the world.

Chairman (now former CEO) Mark Leonard is humble, honest and transparent in his annual letters, not unlike Warren Buffett. This is one of the inspirations when you look at the business model and tone in the annual letters.

Mark Leonard has been an incredible capital allocator. He has put in place a sophisticated process for identifying, evaluating and integrating acquisitions.

Every employee who works at Constellation is considered, can grow and is incentivized through a meritocratic organization and a share in the company's results. There's a reason that over 99% of employees recommend President and former CEO Mark Leonard (Glassdoor rating).

Looking at what he's done since his early days as founder and CEO, it's all geared towards creating long-term shareholder value without sacrificing the company's culture and sustainability.

The management team is adamant about not diluting shareholders, as the shares outstanding today are around 21 million, and this number has not grown since the IPO. The core shareholder base at the time of the IPO hasn't really changed. Mark Leonard still owns 430,282 shares, worth over $900 million.

In figures

Constellation Software is (end 2022) :

- Gross margin: 34.3%

- EBITDA margin: 15.7%

- Operating margin: 13.3%

- Net margin: 7.7%

- FCF margin: 19

- FCF Conversion (EBITDA): 73.8

- ROE: 39.7% EBITDA

- ROA: 10.3% OF SALES

- ROCE: 31.1% OF SALES

- CAPEX/CASH FLOW: 0.62

- Debt/EBITDA: 0.87x

- Sales growth (CAGR) over 10 years: 21.9

- EPS growth (CAGR) over 10 years: 18.4%

- Performance (CAGR) over 5 years (with dividends): 27.1

- Performance (CAGR) over 10 years (with dividends): 35.1%

- Performance (CAGR) since IPO (with dividends): 35.9

- FCF Yield: 3.64%

| Fiscal Period: December | 2019 | 2020 | 2021 | 2022 | 2023 | 2024 | 2025 |

|---|---|---|---|---|---|---|---|

| Net sales 1 | 3,490 | 3,969 | 5,106 | 6,622 | 8,407 | 10,111 | 12,099 |

| EBITDA 1 | 934 | 1,231 | 1,512 | 1,701 | 2,209 | 2,740 | 3,252 |

| EBIT 1 | 511 | 723 | 873 | 882 | 1,188 | 1,539 | 1,906 |

| Operating Margin | 14.64% | 18.22% | 17.1% | 13.32% | 14.13% | 15.22% | 15.75% |

| Earnings before Tax (EBT) 1 | 456 | 603 | 374 | 725 | 265 | 1,208 | 1,505 |

| Net income 1 | 333 | 436 | 310 | 512 | 565 | 591.9 | 693.9 |

| Net margin | 9.54% | 10.99% | 6.07% | 7.73% | 6.72% | 5.85% | 5.74% |

| EPS 2 | 15.73 | 20.59 | 14.65 | 24.18 | 26.67 | 33.98 | 42.38 |

| Free Cash Flow 1 | 733 | 1,161 | 1,271 | 1,256 | 1,737 | 2,207 | 2,638 |

| FCF margin | 21% | 29.25% | 24.89% | 18.97% | 20.66% | 21.83% | 21.8% |

| FCF Conversion (EBITDA) | 78.48% | 94.31% | 84.06% | 73.84% | 78.63% | 80.54% | 81.13% |

| FCF Conversion (Net income) | 220.12% | 266.28% | 410% | 245.31% | 307.43% | 372.86% | 380.16% |

| Dividend per Share | 24.00 | 4.000 | 4.000 | - | - | - | - |

| Announcement Date | 2/13/20 | 2/12/21 | 2/10/22 | 3/29/23 | 3/6/24 | - | - |

Conclusion

We are dealing here with an extremely qualitative company, led by an honest, competent and skin-in-the-game management team, whose fundamentals (growth, profitability, profitability, financial health, business model stability, etc.) are among the best in any category/sector. The valuation is demanding when we look at traditional ratios (P/E 2022 of 64.5x) but much less so when we talk about cash flow (FCF Yield of 3.64%, i.e. 27.5x its free cash flow). Time will tell whether Mark Leonard and his team deserve this valuation. If the story continues as it has, the P/E ratio will soon be forgotten in favor of growth and profitability, which could quickly catch up with the valuation requirement...

Find out more about the other episodes in the Multibagger Stories series: