Effective

Effective

Overview of the Requirements

The purpose of the revised requirements was, in part, to prevent landlords from maintaining residential properties below acceptable standards and later anonymously hiding behind the entity owning the real property.4 The Amended Filing Requirements, however, apply to all entities in DC (such as corporations, limited liability companies, partnerships, nonprofit corporations and unincorporated nonprofit associations)5, and not just those engaged in the ownership and operation of residential real estate.

The Initial Amendment to the DC Code expanded §29-102.01 to require that entities filing for a new domestic or foreign registration (or for existing entities, submitting mandatory biennial reports to DCRA), provide the (i) name, (ii) residence and (iii) business address of each person whose:

(6) . . . aggregate share of direct or indirect, legal or beneficial ownership of a governance or total distributional interest of the entity:

(A) Exceeds 10%; or

(B) Does not exceed 10%, provided, that the person:

(

(ii) Has the ability to direct the day-to-day operations of the entity.

The later enacted Amended Filing Requirements were drafted to ensure compliance by foreign entities and clarify that, they too, need to undergo the same analysis. The added provision provides that such entities will also be required to provide the (i) name, (ii), residence and (iii) business address of each person whose:

(7) . . . aggregate share of direct or indirect, legal or beneficial ownership of a governance or total distributional interest of theforeign entity:

(A) Exceeds 10%; or

(B) Does not exceed 10%, provided, that the person:

(

(ii) Has the ability to direct the day-to-day operations of the foreign entity.

In a prior version to the Amended Filing Requirements6, the Council specifically stated their 'rationale' for such amendment was to clarify the Council's intent to ensure businesses incorporated outside of DC, that have an ownership interest in entities doing business in DC, disclose the required ownership information to the DCRA.

Potential Consequences

Significant consequences may now exist for entities that fail to meet the requirements of the Amended Filing Requirements.

The result of a failure to comply with the new amendments, of course, goes beyond potential exposure to statutory penalties. If entities are dissolved, for example, a borrower is likely to risk defaulting under typical loan documents which require the record owner of real property to remain registered at all times to do business in DC. Given the subjective nature of whether the requested information has been 'properly' disclosed, and without knowing whether DC will require supporting evidence (including otherwise highly confidential organizational documents), the Amended Filing Requirements present a significant concern.

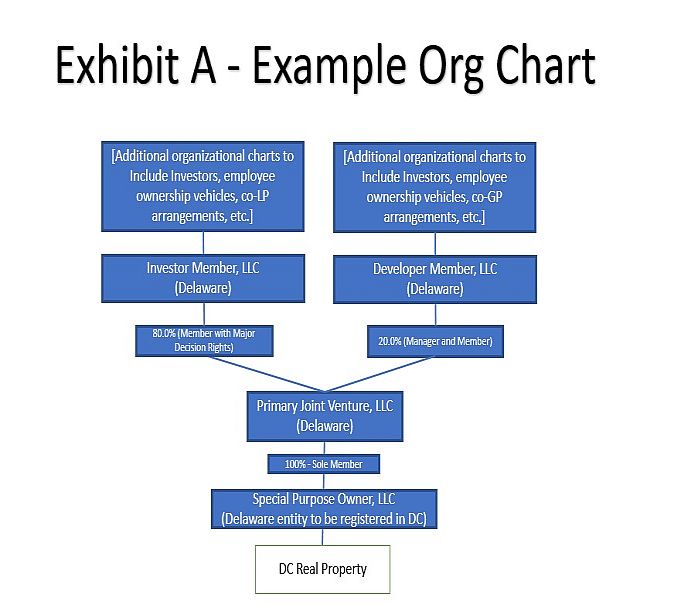

Moving forward, companies should explore these issues before registering to conduct business or filing biennial reports in DC. A sample organizational chart for a real property owning limited liability company required to register in DC, and some of the questions raised thereby, can be found on Exhibit A below.

Additional Thoughts

- Our assumption is that the filing entity (

Special Purpose Owner, LLC ) is required to report each owner meeting the requirement ofD.C. Code § 29-102.01, which would include all applicable entities going up the chain of ownership. In the above example, this would mean that at least (i)Primary Joint Venture LLC , (ii) Developer Member and (iii) Investor Member would be considered a greater than 10% owner. In a typical deal structure, additional persons or entities on the Investor Member side (and possibly on the Developer Member side) would also meet this test. -

The concept of control in paragraphs (6) and (7) of

D.C. Code § 29-102.01 is broad enough to cause confusion when analyzing entities acquiring commercial real properties in DC (including REIT subsidiaries or other large commercial real estate developers), which typically have complex organizational structures. The control test raises additional questions, including:

A. If Developer Member is designated as the Manager in the Operating Agreement of

B. Does each entity in the chain with 'control' over the primary joint venture members also have to report having control? In other words, would the control test be reviewed in the same manner as the ownership test (where control is tested at every level of the chain of ownership)?

*

Footnotes

1

2 See generally

3 D.C. Act 23-203. Fiscal Year 2020 Budget Support Clarification Amendment Act of 2020.

4 Katie Arcieri. "

5

6 Bill 23-504. Fiscal Year 2020 Budget Support Clarification Amendment Act of 2019.

7

8 Fiscal Year 2020 Budget Support Clarification Amendment Act of 2020. § 29-102.01(a)(8).

9 Fiscal Year 2020 Budget Support Clarification Amendment Act of 2020. § 29-102.11(8).

Originally published by

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.

Mr

Arnold & Porter

601 Mass. Ave., NW

DC 20001-3743

Tel: 202942.5000

Fax: 202942.5999

E-mail: Anna.shelkin@apks.com

URL: www.arnoldporter.com

© Mondaq Ltd, 2020 - Tel. +44 (0)20 8544 8300 - http://www.mondaq.com, source