EARNINGS/SALES RELEASES

Chargeurs reported results well below our expectations and aligned with consensus regarding both the top-line and profitability for H1 23, solely due to the cyclical weakness of the industrial protection film business. On the other hand, the Museum Studio division is firmly establishing itself as a group’s new growth lever within the Luxury division. Also worth noting is the good momentum of the group’s new growth drivers, which now account for nearly 60% of group revenue. The drop in profitability, compounded by a significant increase in financial expenses (net debt reaching €194.4m secured by ample credit lines), led to a sharp fall in the group’s net profit to €3.3m (vs. €10.2m).

FACT

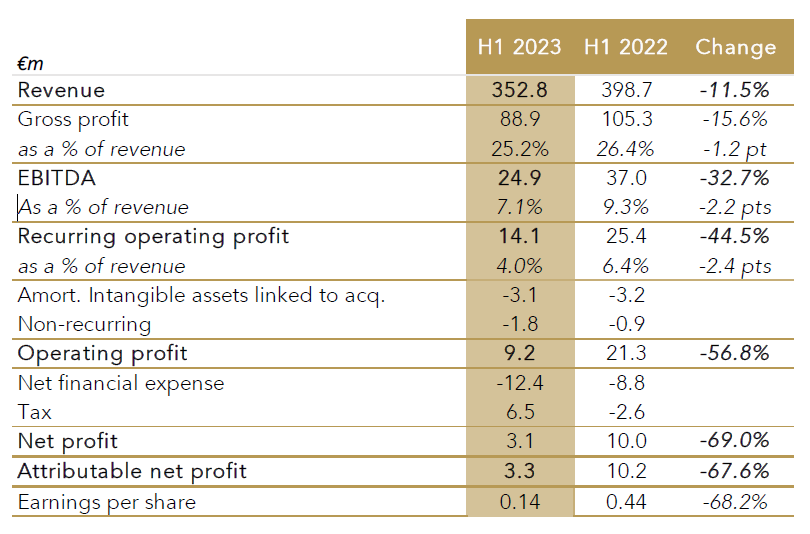

- Chargeurs posted H1 total sales of €352.8m, down 12% organically yoy, driven by a 23.1% organic decline in Advanced Materials (new name for industrial protection film) sales to €146.7m and the pullback of Healthcare Solutions, now irrelevant.

- The Chargeurs Museum Studio division reported a strong increase in sales (+48.5% organic growth yoy) to €61.2m.

- In H1 23, Chargeurs reported a 44.5% fall in operating profit to €14.1m, against a consensus of €15.8m.

- Chargeurs recorded an increase in CFO to €4m versus €0.3m due to lower working capital requirements than in H1 22.

- After capital expenditures and dividends paid for FY-22, cash flow was down by €18m, bringing net debt to €194.4m at the close, corresponding to a leverage ratio of 3.5x.

-

Despite these disappointing results, Chargeurs cautiously expects a gradual rebound in its Advanced Materials division, which should enable it to achieve group global sales of €800m by 2024 and an EBITDA margin in the range of 9-10%.

ANALYSIS

Let’s start by prefacing that Chargeurs Advanced Materials (CAM) division is a macro proxy. In 2021, the division had an exceptional year, with inventories built up by customers wishing to manage supply-chain disruptions in a post-COVID environment. CAM has since faced a significant destocking effect. Although the destocking trend seems to be over, industrial customers remain cautious about the near-term outlook with two pain points: construction at large and Germany. Group sales down 12% organically led to a 44.5% yoy fall in operating profit to €14.1m in H1 23.

Chargeurs Advanced Materials reported a 23.1% yoy organic decline in sales to €146.7m. The contraction in sales, in H1 23, was due to lower industrial volumes from customers in the context of energy and inflationary shocks. The division was also penalised by the crisis in the real estate and new construction markets (which account for 25% of its sales). As a result, CAM recorded a 74.4% fall in operating profit to €4.1m, although it successfully remainded positive thanks to a flexible organisation and a breakeven point lowered during recent years. Nevertheless, Chargeurs remains confident that business will inevitably pick up again, as the structural demand for industrial film protection is high and will be driven by i) the end of customer destocking, and ii) growth levers such as industrial equipment, renovation, mobility equipment, high-end household appliance and industrial building markets. It looks as if CAM has not pushed prices beyond the mix effects.

While Chargeurs Fashion Technologies (CFT-PCC) excluding Healthcare Solutions recorded a slight decline in sales 1.3% lfl to €100.5m, the division posted a slight improvement in margin of 0.4ppt to 7.2%. CFT PCC benefited from a favourable customer/product mix coupled with pricing power that enabled it to pass on raw material and energy costs to customers. The division is clearly being pulled by technical textiles for the garment industry among the end-markets and pulled by profitability gains in the organisation.

Chargeurs Museum Studio (CMS) achieved a clear beat on our expectations, with organic sales growth of 48.5% to €61.2m against €50.5m expected (€51.9m consensus). Top-line growth was driven by the gradual start-up of projects won in 2021 and 2022. The division’s operating income doubled in H1 23 (vs. H1 22) to €3.8m (vs. €1.8m), bringing the operating margin to 6.2% (up 1.2 ppt). The outlook is promising for the division, which should feel the full effect of the projects won in late 2021 and 2022, with deliveries by late 2023, 2024 and 2025. Chargeurs has confirmed its sales outlook of €120m for 2023 and €150m for 2024. This is an impressive achievement for a business started from scratch.

Chargeurs Personal Goods, Chargeurs’ new division representing its ambition towards Quiet Luxury through Altesse Studio and Cambridge Satchel, got off to a good start with H1 23 sales of €4.1m and an operating margin of 4.9%. Chargeurs expects the group’s visibility to increase with i) the opening of Swaine’s flagship store on New Bond Street, London, in June, ii) the use of its products by the film industry, notably Indiana Jones’ Stetson for Swaine, and iii) the visibility linked to the coronation of King Charles III.

All is not rosy for the Luxury division, however, with a 25.2% yoy organic decline for Chargeurs Luxury Fibers (CLF) which was negatively impacted by the cyclone that struck New Zealand in February 2023. Despite the decline in top-line growth, CLF nonetheless reported an increase in operating profit to €1.2m, corresponding to margin growth of 1.2 ppt. The division continues to be driven by the roll-out of NATIVA, its blockchain based tracking tools and associated confidence about origins, which is increasingly relied upon by major brands.

Despite the 32.7% drop in EBITDA to €24.9m, the reduction in working capital requirement to €3.2m (vs. €17.8m) led to cash flow generation from operations of €4m, compared with €0.3m in H1 22. However, after capex and the dividend paid for 2022, the net debt position deteriorated from €174.7m in FY-22 to €194.4m in H1 23, increasing the leverage ratio to 3.5x. In addition, the environment of rising interest rates coupled with hyperinflation in Argentina resulted in an increase in financial expenses from €8.8m to €12.4m. Chargeurs’ average interest rate on its debt might end up being a significant 10% for 2023 (Chargeurs, on the other hand, expects it to be 5%), presumably as the price to pay for ample credit lines.

In line with higher financial expenses and lower profitability, Chargeurs posted net income down 69% yoy in H1 23 to €3.3m.

Assuming a gradual recovery in CAM, Chargeurs aims to achieve sales in excess of €800m in 2024 with an EBITDA margin of 9-10%.

All in all, notwithstanding the decline in CAM and in the group’s industrial activities, we regard Chargeurs’ paradigm shift and premiumisation in a very positive light, as demand and margin shocks on CAM activities such as the one recorded in H1 23 would have been of much greater stress less than 10 years ago.

IMPACT

We will be trimming our FY23 estimates, particularly for CAM, following this release.