EARNINGS/SALES RELEASES

Chargeurs continued to be negatively impacted by a still-difficult environment for its various businesses in the Q3 23, with a 7.6% organic decline in revenues. However, the worst now seems to be over as the recovery in the Advanced Materials division is showing signs of picking up pace, with the monthly volumes in September and October higher than in 2022. Meanwhile, Chargeurs Museum Studio continues to assert itself as a new growth driver. The 2024 targets were reaffirmed.

FACT

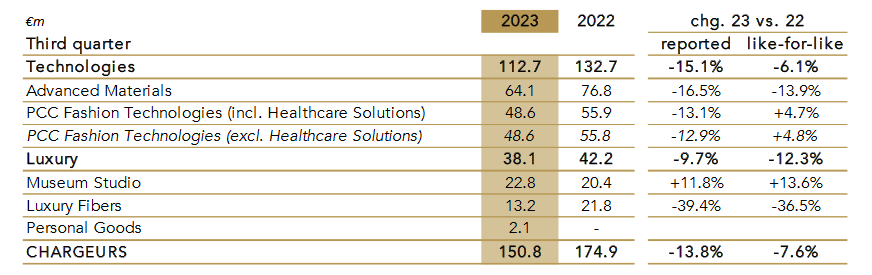

- Chargeurs posted organic sales down 7.6% yoy to €150.8m in Q3 23, penalized by its Chargeurs Advanced Materials (ex-Protective film) and Chargeurs Luxury Fibers (CLF) businesses.

- The Technology and Luxury divisions posted organic declines of 6.1% and 12.3% respectively in the quarter, with sales of €112.7m and €38.1m.

- In Q3 23, Chargeurs Advanced Materials recorded a 13.9% organic yoy drop in revenues to €64.1m which, in addition to being penalized by a difficult market, experienced a seasonality effect in August.

- Chargeurs Luxury Fibers also recorded a sharp decline, -36.5% organic yoy, to €13.2m due to a negative price effect (strong drop in the conventional wool price (i.e.: micron 17 down -30% on Q3 and -21% for 9M 23), and a change in product mix (less conventional and rising certified Nativa wool), which Chargeurs does not expect to negatively impact the gross margin, as conventional sales have a lower margin compared with certified wool.

- On the other hand, the Museum Studio (CMS) business appeared robust, with 13.6% organic growth yoy and revenues of €22.8m for the quarter.

- Chargeurs reaffirmed its 2024 outlook of sales in excess of €800m, an EBITDA margin of between 9% and 10% and a Debt/Ebitda multiple of less than 3x.

ANALYSIS

Chargeurs continues to be hampered by a challenging environment in 2023, which translated into a 7.6% yoy organic sales decline to €150.8m in the Q3. As mentioned before, the biggest underminer of Chargeurs’ performance is its macro proxy, Chargeurs Advanced Materials (CAM). Having enjoyed an exceptional 2021, boosted by an inventories build-up by clients, the business has had to contend with a destocking effect since 2022. That said, the division has now passed its nadir.

In Q3 23, CAM reported a 13.9% yoy organic decline in revenues to €64.1m. While at first sight such a contraction may appear negative, it is actually positive when set against the 27% yoy lfl decline in the Q1 23 and the 19.2% yoy lfl decline in Q2-23. In spite of the complex market conditions and a seasonal August, volumes picked up in October for the fifth consecutive month, exceeding those recorded in the same period in 2022. The volume upturn in all regions – Asia, EMEA and the Americas – bears witness to an upswing.

While Chargeurs PCC Fashion Technologies (CFT PCC) reported a 12.9% yoy decline in absolute revenues in Q3 23 to €48.6m, the division recorded a 4.8% organic increase in revenues. CFT PCC enjoyed a positive price effect stemming partly from the hyperinflationary situation in Argentina, together with a favourable volume effect in Asia. Chargeurs does not seem concerned by the slight decline in European sales in Q3, as CFT PCC is planning to expand its global network across all apparel segments with an increasing market share.

Following on from the H1 23, Chargeurs Museum Studio (CMS) further asserted itself as the Group’s new growth lever, with revenues up 13.6% yoy to €22.8m, taking 9-month yoy organic growth to 35.9% with revenues of €84m. The division’s momentum continues to be positive with worldwide projects in the pipeline. Quite an impressive performance, bearing in mind the fact that the business was built from scratch, which led to the reiteration of the revenue guidance of €120m in 2023 and €150m in 2024.

Chargeurs Luxury Fibers (CLF) reported an organic yoy decrease of 36.5% with sales of €13.2m in the Q3 23 compared with €21.8m last year, due to lower conventional wool prices. Having said that, Chargeurs intends to pursue the premiumization of its business with growing sales linked to sustainable wool, Nativa, now accounting for 20% of sales versus 10% last year, a trend that is expected to enable CLF to maintain its operating margin.

The Chargeurs Personal Goods division recorded a sound first set of 9-month figures, with revenues of around €6.2m. We don’t have a reference year, since the Cambridge Satchel and Altesse Studio brands were consolidated in December 2022, but we can however assert that the outlook for the division is good, with new partnerships expected for the Cambridge Satchel and new distributors, including Galeries Lafayette, for Altesse Studio.

Recent developments in terms of volumes suggest that CAM’s gradual recovery scenario is materializing, which we regard as a clear positive. Chargeurs thus confirmed its 2024 objectives of sales in excess of €800m, with an EBITDA margin of 9-10% and a debt/EBITDA multiple of less than 3x.

IMPACT

Our estimates are likely to remain broadly unchanged, although we are likely to revise downwards our revenue estimates for Chargeurs Luxury Fibers.